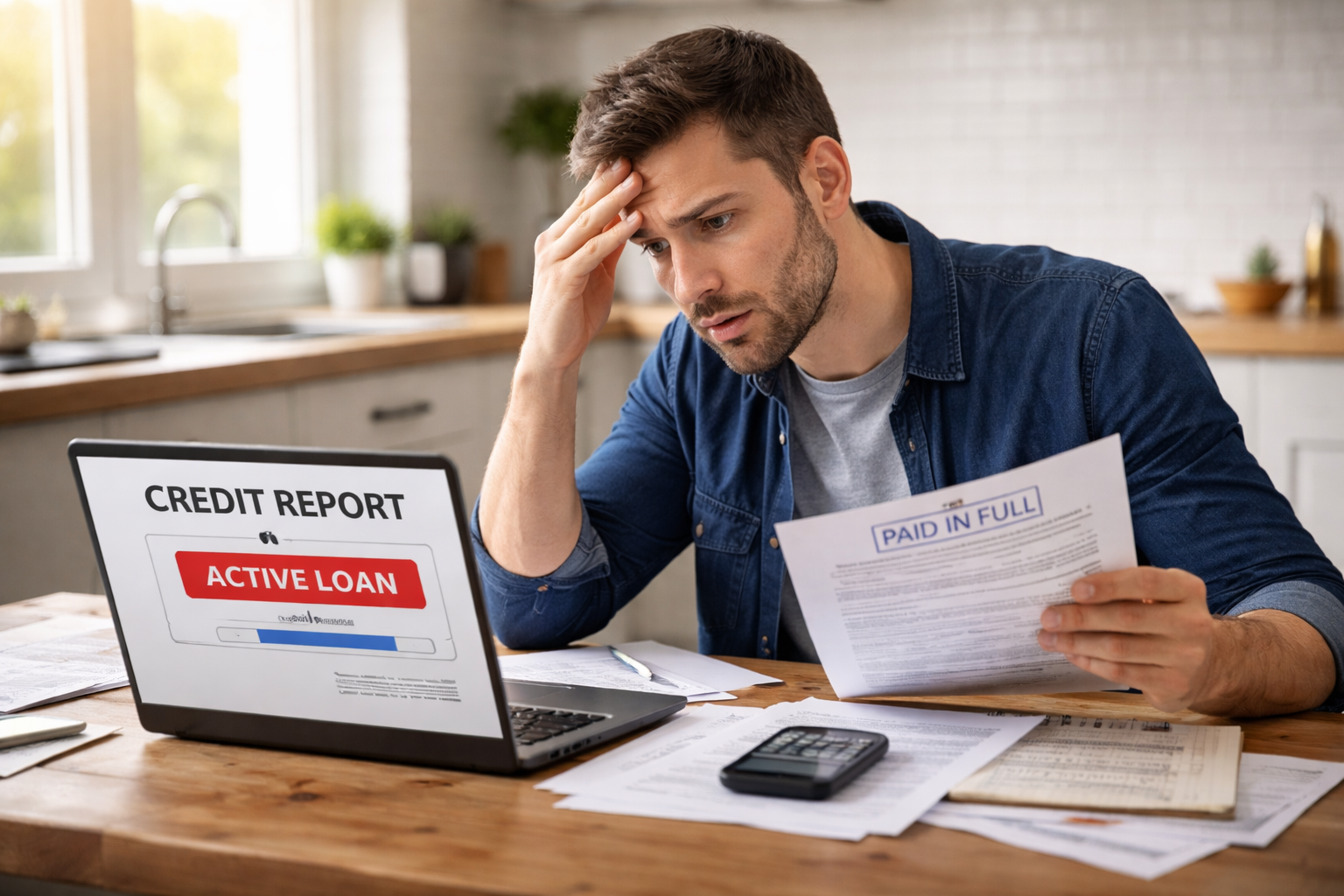

Dealer failed to report loan payoff to credit bureau after full payment was the phrase I kept repeating in my head the morning I opened my credit report and saw the account still sitting there like I owed something. I had already made the last payment. I was not guessing. I was not early in the process. I was done. The money had left my account, the amount matched what I had been told, and I expected the record to close out quietly in the background. Instead, the loan still looked alive enough to create a problem.

The worst part was that nothing dramatic had happened on payoff day. No one warned me there was a hold. No one said the account was waiting on another adjustment. No one told me the final reporting piece could lag behind the actual payoff. I only found out because I checked before moving on to the next financial step. A loan can be fully paid in one system and still appear unresolved in the system that lenders and credit bureaus rely on. That gap is where this problem starts costing people real time, real approvals, and real negotiating power.

Before going deeper, it helps to understand how dealership finance problems often keep going after the papers are signed. This related piece gives that broader context.

Why a Paid Loan Still Looks Unpaid

Dealer failed to report loan payoff to credit bureau after full payment sounds simple, but in the real world it usually happens because the payoff and the reporting move through different channels. A dealership employee may collect payoff funds, quote the amount, promise closure, or tell you everything is handled. But the actual credit reporting may be done by the lender, servicer, or another furnishing entity sending data to the bureaus on a cycle. That separation is why people keep hearing two different stories. The dealer says the loan is finished. The report says otherwise.

That does not mean the dealer is irrelevant. In many auto finance problems, the dealer is the reason the chain broke. The store may have given the wrong payoff amount, delayed transmitting documents, mishandled a cancellation refund, sent incorrect account details, or failed to follow through after telling the customer the account would be closed properly. When the consumer hears “you are all set,” that statement usually combines several separate back-end tasks that may not all have been completed.

Sometimes the final payment posts but the status does not change. Sometimes the loan balance reaches zero internally but the tradeline remains marked as open. Sometimes the account should have been updated after a GAP or warranty refund, but that credit was still floating around in another queue. In other situations, the account is reported correctly to one bureau and incorrectly to two others. The result looks the same from the consumer side: the loan was paid, but the report still tells a worse story.

If the account shows a zero balance but still looks open:

The issue may be the closure status, not the payoff itself. The account may need to be updated as paid in full or closed by consumer.

If the account still shows money owed:

The reporting chain may not have absorbed the final payment at all, or a refund, fee, or residual amount may have been handled incorrectly.

If the account shows late history after payoff:

You may be dealing with a more serious furnishing error, especially if the final payment timing was misread or posted late on the reporting side.

If one bureau looks right and another looks wrong:

The problem may be limited to one reporting stream, which means you cannot assume a single correction will fix everything automatically.

What You Need to Match Line by Line

Dealer failed to report loan payoff to credit bureau after full payment is much easier to fix when you stop talking about it in general and start matching dates, balances, and status fields. A lot of people lose momentum because they keep saying, “I paid it off,” without organizing the proof in a way that forces the other side to deal with the exact error. You need to line up the transaction record and the tradeline record side by side.

Start with the bank record showing when the final payment actually cleared. Then compare that date with any payoff letter, zero-balance statement, online account screenshot, email confirmation, or lender notice you received. After that, compare those records to the credit report entry itself. Look closely at the balance, payment status, account status, date updated, and any notation showing whether the loan is open, closed, current, late, or paid. Those fields matter more than the overall feeling that the account “looks wrong.”

If the balance is zero but the account still appears active, your dispute should focus on status and closure notation. If the balance is not zero, your dispute needs to focus on incorrect outstanding debt reporting. If the account shows a past-due amount, delinquency, or ongoing payment obligation after the full payoff, that is a more urgent problem because it can affect underwriting decisions in a different way. The fastest disputes are the ones that identify exactly what is inaccurate instead of arguing with the entire tradeline at once.

Where the Breakdown Usually Happens

Dealer failed to report loan payoff to credit bureau after full payment usually comes from one of a few predictable breakdown points. Understanding them helps you direct pressure where it belongs.

One common version starts with the payoff amount itself. The customer pays what the dealer or finance office says is the final amount, but the figure was based on an outdated quote, a timing gap, or a pending adjustment. The customer thinks the account is closed. The lender system thinks there is a remaining amount, even if it is small. Months later, the tradeline still does not reflect a proper paid-in-full closure because the account was never fully reconciled.

Another version involves cancellations tied to the loan. A dealer may say a warranty cancellation, service contract refund, or GAP refund will be applied and bring the balance down correctly. The customer hears that the loan will be resolved. But the refund arrives late, goes to the wrong ledger path, or is never linked properly to the reporting cycle. On paper, the loan payoff and the reporting update fall out of sync.

A third version happens after a trade-in, refinance, or rewritten contract. The customer believes the old debt is gone because a new transaction replaced it. But the prior loan is not fully closed out on the reporting side. This is where people get confused because the dealership treats the old loan as a completed step in the sale, while the reporting world still sees an unresolved account.

A fourth version is pure lag mixed with poor communication. The payment posted, but no one told the customer how long bureau reporting might take, which entity is furnishing the data, or what documents prove the account is truly closed. By the time the customer notices the problem, everyone starts pushing responsibility elsewhere.

Payoff quote problem:

You paid the number you were given, but it did not fully satisfy the account because of timing, interest, or pending adjustments.

Refund application problem:

A cancellation refund was supposed to reduce or close the loan, but the credit never lined up properly with the reporting record.

Deal transition problem:

A trade-in, refinance, or contract rewrite created the appearance of closure before the previous loan was fully updated.

Reporting-cycle problem:

The loan payoff happened, but the bureau furnishing cycle did not reflect it accurately or completely.

Data match problem:

The right payment exists, but it is not tied cleanly to the right account details in the reporting chain.

When the Dealer Is More Than a Bystander

Dealer failed to report loan payoff to credit bureau after full payment is sometimes described as if the dealer had nothing to do with the bureau issue because “the lender reports, not us.” That can be partly true and still misleading. If the dealership quoted the payoff, accepted money based on that quote, handled related cancellations, promised that the account was settled, or controlled the paperwork that should have triggered the next step, the dealer may be central to the problem even if it is not the final furnisher.

This matters because many consumers waste days arguing with whichever company picks up the phone first. If the dealer was involved in the final resolution of the loan, you need written answers from them. Ask for the exact payoff handling trail. Ask when the payoff was transmitted, to whom it was transmitted, which account number was used, whether any add-on cancellations were involved, and which entity is responsible for furnishing the account status to the credit bureaus. Those are not abstract questions. They force the dealership to move from vague reassurance to verifiable facts.

If the payoff issue is tangled up with a trade-in or older financed vehicle, this related article can help you trace the earlier failure that often sits underneath the reporting problem.

What to Do Depending on What You See

Dealer failed to report loan payoff to credit bureau after full payment does not look the same in every file. The strongest approach is to sort yourself into the version closest to your own situation and act accordingly.

Your report shows zero balance, but the loan still looks open:

Push for correction of the account status and closure notation. This often means the payoff posted but the final status update never moved through correctly.

Your report still shows a balance due:

Lead with proof that the final payment cleared, then add any payoff statement or zero-balance notice. Ask specifically for correction of the reported balance and account status.

The report shows late or past-due amounts after full payoff:

This is more serious because it suggests the payment history or timing was reported inaccurately, not just the closure field. Separate that issue clearly in your dispute.

You paid after being told a refund or cancellation would be applied:

Ask where that refund went, when it posted, and whether the account was ever fully reconciled before bureau data was sent.

You are about to apply for a mortgage, refinance, or another auto loan:

Do not wait quietly for the next reporting cycle. Build the dispute packet immediately and send it while also requesting dealer documentation in writing.

Only one bureau is wrong:

Treat that as a real dispute with that bureau. Correction on one report does not guarantee correction on the others.

The dealer blames the lender and the lender blames the dealer:

Stop waiting for them to decide whose fault it is. Dispute with the bureau and furnisher, and separately demand the dealer’s payoff transmission records.

Build a Clean Dispute Packet

Dealer failed to report loan payoff to credit bureau after full payment becomes much easier to resolve when your paperwork is clean. A messy file gives everyone room to delay. A focused file narrows the issue and makes it harder to dodge.

Your packet should include a marked copy of the credit report showing the inaccurate auto loan entry, proof that the final payment cleared, and any document showing the account should be paid in full or closed. That may be a payoff statement, final account screenshot, confirmation email, letter showing zero balance, or any written communication from the dealer or lender saying the loan was satisfied. Add a short timeline listing dates in order. Keep it plain. Do not turn it into a long emotional summary of the entire dealership experience unless those details directly explain the payoff error.

The explanation should be simple: the account was paid in full on a specific date, the credit report still reflects inaccurate balance or status information, and you want the tradeline corrected. Focus on what is wrong and what documents prove it. That discipline matters. Many consumers weaken their own dispute by mixing ten different complaints into one file.

For the one official source in this article, use the CFPB’s guidance on disputing credit report errors with both the credit reporting company and the company that furnished the information: official CFPB dispute guidance.

What People Do That Delays the Fix

Dealer failed to report loan payoff to credit bureau after full payment often stays unresolved because the first response from the consumer is understandable but weak. They call, they explain, they get told to wait, and they assume the update is already in motion. Then nothing happens.

One common mistake is relying on phone conversations alone. Verbal reassurance feels productive because a person sounds helpful, but it does not create a clear record. Another mistake is sending proof of payment without proof that the loan should actually be marked paid in full. A bank screenshot can show money moved, but it may not show that the loan was fully satisfied unless you pair it with the payoff record.

Another delay happens when people challenge the entire account history instead of isolating the actual error. If the real problem is that the loan should be closed with a zero balance, say that directly. Do not make the dispute wider than it needs to be. A final mistake is waiting too long because someone said reporting “takes time.” Sometimes it does. But passive waiting is not a strategy, especially if you need your report cleaned up before a new application.

The biggest practical mistake is assuming a fully paid loan and an accurately reported paid loan are the same thing. They are not the same thing when another lender reviews your file.

Key Takeaways

- Dealer failed to report loan payoff to credit bureau after full payment is usually a breakdown between payoff processing and credit furnishing, not just a random annoyance.

- You need to identify whether the error is balance, status, closure notation, delinquency history, or a mix of these.

- The strongest proof set is payment clearance plus payoff proof plus the marked credit report entry.

- If the dealer handled the payoff process or promised the account was resolved, ask for the exact payoff transmission trail in writing.

- Do not wait passively if a major credit decision is coming soon.

FAQ

Can a paid auto loan still stay on my credit report?

Yes. The issue is usually not whether it appears at all, but whether it appears accurately. A paid, closed account can remain on a credit report. The problem is when it still shows the wrong balance, wrong status, or wrong payment condition.

Should I contact the dealer, lender, or credit bureau first?

In many situations, you should not treat those as either-or choices. If the dealer handled the payoff process, contact the dealer in writing. If the lender or servicer is the furnisher, dispute with that company too. And if the report is inaccurate, dispute with the bureau showing the error.

What if the account is paid but still marked open?

That often means the balance may have updated but the closure status did not. Your dispute should ask for correction of the account status and paid-in-full closure notation.

What if I am about to apply for another loan?

Move faster, not slower. Build the dispute packet immediately and push for written confirmation of the payoff and the furnishing path. Waiting for the next cycle without documentation can cost you time you do not have.

Will one corrected bureau update the others automatically?

Not always. If the loan looks accurate on one report and inaccurate on another, you still need to address the incorrect report directly.

What to Read Next

If your payoff reporting issue is tied to title cleanup or post-loan paperwork, this is the next article to open because those problems often move together.

Dealer failed to report loan payoff to credit bureau after full payment can look like a small technical problem from the outside, but it often becomes serious at exactly the wrong moment. People usually find it when they are trying to move forward, not when they have extra time to deal with another paperwork mess. That is why this issue feels so disproportionate. You did what you were supposed to do. You paid the loan. But the record that matters to the next lender may still be stuck in the wrong place.

Do not let the file sit there while different companies keep telling you to wait. Pull the report, identify the exact field that is wrong, attach the payoff proof, send the dispute, and demand the dealer’s written payoff trail if the dealership was part of the final resolution. If the loan was fully paid, the reporting should say that clearly, and you should keep pushing until the record matches reality.