Dealer Changed Vehicle Price on Final Purchase Contract was the exact thought that hit me when the finance manager turned the document toward me and started pointing at signature lines instead of the numbers. Up until that moment, the deal had felt settled. We had gone back and forth on price, the salesperson had written everything down, and I had already reached the point where I was picturing the drive home. Then I looked down at the final purchase contract and saw that the vehicle price was higher than the number we had been discussing all afternoon.

What made it worse was how ordinary the moment looked. Nobody announced a change. Nobody explained that the numbers had been revised. The tone in the room stayed casual, almost rushed, like I was expected to keep moving and sign before I had time to think. That is why Dealer Changed Vehicle Price on Final Purchase Contract can catch buyers off guard. It often does not arrive as a dramatic confrontation. It shows up quietly, inside paperwork you are expected to sign quickly.

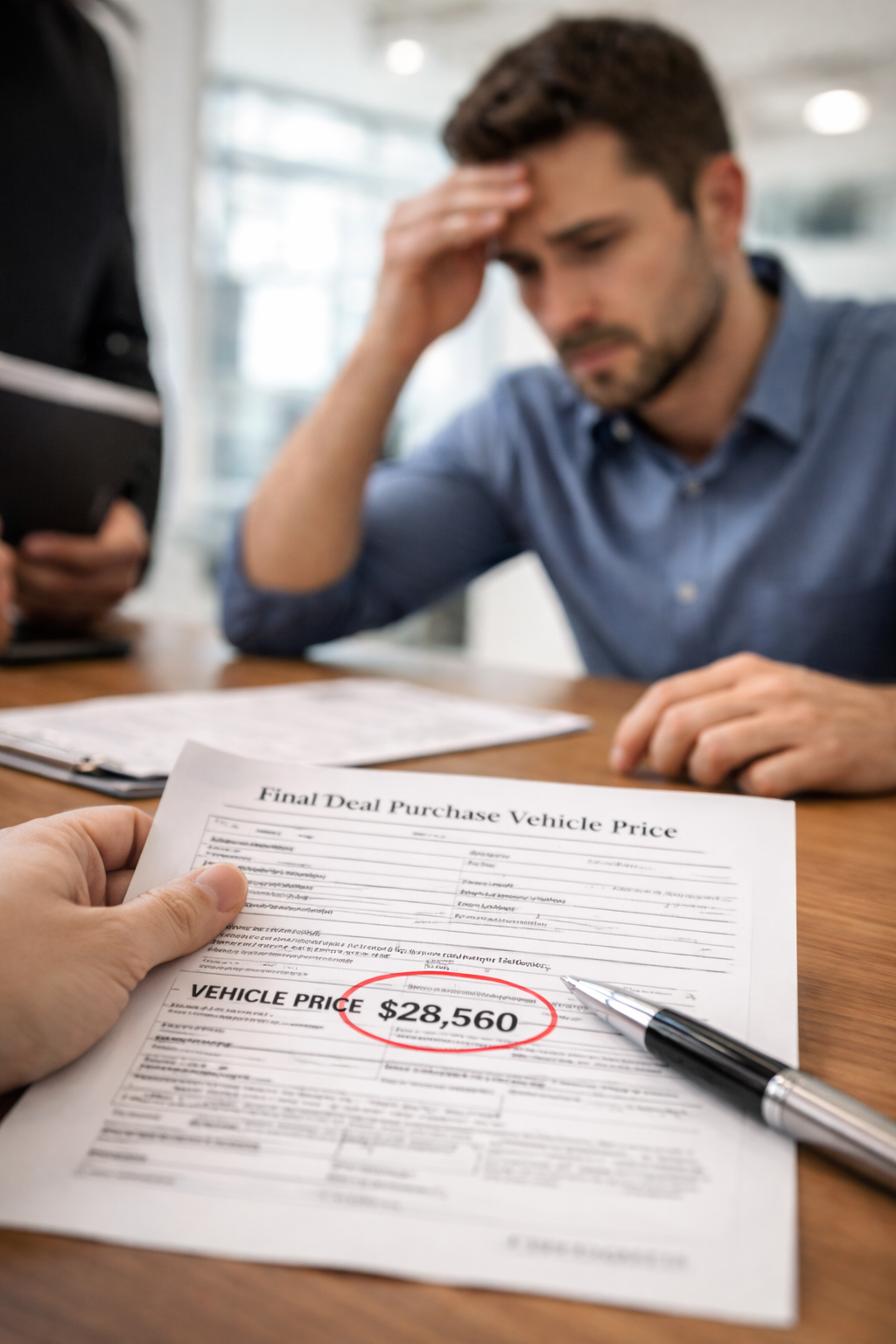

Dealer Changed Vehicle Price on Final Purchase Contract is the kind of problem that causes immediate confusion because the buyer usually has more than one number in mind. There is the number discussed on the showroom floor, the number shown on a worksheet, the number folded into the monthly payment quote, and then the number that appears in the final contract. When those numbers do not match, the dealership may act like it is a simple misunderstanding. In reality, that difference can determine the cost of the entire transaction.

Before going deeper, it helps to review a closely related pricing issue that often happens earlier in the same sales process:

This related guide explains how dealers sometimes introduce extra charges after a verbal or written agreement, which is often the step right before the final contract changes:

How This Usually Starts

Dealer Changed Vehicle Price on Final Purchase Contract usually starts long before the buyer notices it. The customer negotiates with a salesperson first. That part feels straightforward. A price is discussed. A trade-in may be evaluated. A down payment is mentioned. Monthly payment ranges are shown. Sometimes the buyer even receives a printed worksheet with what looks like the agreed vehicle price.

But the real risk begins when the deal moves from the sales desk into the finance office. That is the transition point where numbers can be rebuilt, packaged, bundled, or re-entered into the dealership system. The buyer often assumes that the finance office is simply printing the same deal in final form. That assumption is exactly what creates danger.

Dealer Changed Vehicle Price on Final Purchase Contract tends to appear during this handoff. The buyer is tired, the dealership is controlling the pace, and attention gets pulled toward monthly payment, interest rate, warranty options, and signature timing. The more distractions built into the closing process, the easier it becomes for a different vehicle price to slip into the final contract.

Why Dealers Change the Price in Final Paperwork

Dealer Changed Vehicle Price on Final Purchase Contract does not always happen for a single reason. Some situations are caused by sloppy internal processes. Others are more deliberate. The problem for the buyer is that the effect is the same either way: the final contract may no longer reflect the deal that was understood earlier.

One common reason is that the dealership treats the worksheet and the contract as separate stages rather than as the same binding deal. The worksheet may show a negotiated selling price, but the final contract may be generated from the stock record, dealer software defaults, accessory packages, or manager adjustments. If nobody actively checks the final numbers line by line, the contract can come out different.

Another reason is add-on blending. Instead of listing every extra item clearly in a way the buyer would immediately notice, a dealer may allow some charges to reshape the vehicle price or overall sale structure. That makes the deal harder to compare against the earlier negotiation.

Dealer Changed Vehicle Price on Final Purchase Contract also happens when the dealership knows the customer is already invested. By that stage, many buyers have spent hours inside the dealership, arranged insurance, transferred belongings out of another car, called family members, or mentally committed to the purchase. The pressure to finish becomes part of the closing strategy whether anyone says it directly or not.

What the Finance Office Counts On

Dealer Changed Vehicle Price on Final Purchase Contract becomes easier for the dealership when the buyer focuses on the wrong number. Most buyers are trained to look at monthly payment first. Dealerships know this. If the monthly payment stays within the expected range, many customers will not immediately challenge a higher vehicle price, especially when other terms such as loan length or upfront cash are also shifting in the background.

The finance office also benefits from speed. Documents are stacked. Pages are flipped. Signature lines are marked. The conversation often sounds procedural rather than negotiable. The buyer is subtly moved from decision mode into completion mode. That is a dangerous shift.

If the dealership wants you to move quickly, that is exactly when you should slow the process down. Dealer Changed Vehicle Price on Final Purchase Contract is often discovered only by buyers who stop the conversation, hold the paper still, and compare numbers one by one.

When the Difference Is Hidden Inside the Structure

Dealer Changed Vehicle Price on Final Purchase Contract does not always look obvious at first glance. Sometimes the increase is direct and visible. Other times the difference is hidden in the structure of the deal.

The price line is higher than expected This is the simplest version. The vehicle selling price in the final contract is just higher than the price discussed earlier. The dealership may call it an input mistake, a package adjustment, or a misunderstanding. Even if that explanation is true, you should treat it seriously. The contract still contains the wrong number.

The price looks similar, but extras were rolled in Sometimes the number is higher because unwanted protection products, accessories, appearance packages, or service items were folded into the deal. The contract may not immediately read like a dramatic price change, but the buyer is still paying more than negotiated.

The monthly payment distracts from the total cost Dealer Changed Vehicle Price on Final Purchase Contract may be harder to notice when the dealership makes the payment look acceptable by extending the loan term or adjusting other parts of the financing. The price change is still there, but attention is redirected.

A second version of the deal was generated This is one of the more serious situations. The paperwork may reflect a deal structure that differs from the one the buyer believed was being finalized. That can lead to downstream lender issues, funding disputes, or a complete mismatch between what was signed and what was expected.

If your concern is not only the price but whether the contract itself was changed or submitted differently, review this related situation:

What You Still Control Before You Sign

Dealer Changed Vehicle Price on Final Purchase Contract is serious, but before you sign, you still have leverage. That is the most important reality to keep in mind. The dealership may act like the deal is already done, but if the final contract in front of you does not reflect the agreement you accepted, you are not required to sign it.

At that stage, your strongest tools are simple:

- Stop the signing process immediately

- Ask for the earlier worksheet or negotiated breakdown

- Compare the vehicle price line directly against the prior number

- Ask the finance manager to explain every difference in writing

- Refuse to continue until a corrected contract is produced

Dealer Changed Vehicle Price on Final Purchase Contract becomes much harder to resolve after a signature is placed on the document. Before signing, the issue is still preventable. After signing, it may turn into a dispute about what you agreed to and whether the written contract controls.

Mistakes That Make the Situation Worse

Dealer Changed Vehicle Price on Final Purchase Contract often turns into a much larger problem because buyers make one of several predictable mistakes.

The first mistake is assuming the change can be fixed later. In many situations, later is exactly when your leverage disappears. If the paperwork is wrong now, now is when it must be corrected.

The second mistake is accepting a verbal promise. A finance manager might say the problem will be adjusted after signing, that a correction will be made later, or that the extra amount is temporary until a lender update goes through. Unless that correction appears in the actual contract you are signing, it is not enough.

The third mistake is checking only the down payment and monthly payment. Buyers naturally focus on affordability. The dealership knows this. Dealer Changed Vehicle Price on Final Purchase Contract can hide in a transaction where the payment still looks close to expected because the loan term was stretched or another part of the deal was modified.

A manageable monthly payment does not mean the contract is accurate.

How to Check the Contract Like a Serious Buyer

Dealer Changed Vehicle Price on Final Purchase Contract is less likely to slip through if you treat the signing table like a verification point instead of a closing ceremony.

Look directly at the vehicle selling price first. Do not start with the monthly payment. Then review dealer-installed products, service contracts, maintenance packages, GAP coverage, document fees, taxes, registration charges, trade-in allowance, and loan term. Match each line against what was actually agreed.

If something looks different, do not let the discussion drift into general explanations. Ask a narrow question: Why is this vehicle price different from the number previously agreed? That question forces the issue into a form that is harder to blur.

Dealer Changed Vehicle Price on Final Purchase Contract should also make you re-check related terms because pricing differences often travel with financing changes. A dealer that changes one major number may also be changing another.

What to Do if They Pressure You to Sign Anyway

Dealer Changed Vehicle Price on Final Purchase Contract often comes with social pressure. The dealership may suggest the difference is minor, say the paperwork can be cleaned up later, or imply that you are overreacting. Stay focused on the document in front of you.

You do not need a long speech. You do not need to argue emotionally. You only need to say that the vehicle price in the final purchase contract does not match the agreed deal, and you will not sign until the paperwork is corrected.

If they still resist, walking away is sometimes the clearest signal you can send. The dealership may suddenly become much more willing to regenerate the paperwork once it understands the sale is actually at risk.

Official Source

For general consumer guidance on buying and financing a vehicle, review the Federal Trade Commission resource on car buying and auto financing expectations:

FTC guide to buying a new car and reviewing dealer paperwork carefully.

Key Takeaways

- Dealer Changed Vehicle Price on Final Purchase Contract is not a minor paperwork issue when the final number is higher than the agreed price.

- The finance office is where pricing differences often appear because the final contract is generated there, not on the showroom floor.

- Monthly payment can distract from a higher vehicle price, especially when loan terms also change.

- Before signing, you still have the power to stop the process and demand a corrected contract.

- Never rely on verbal promises that the paperwork will be fixed later.

FAQ

Can a dealer legally present a higher vehicle price in the final contract?

A dealer can present a contract with different numbers, but you are not required to sign a contract that does not match the deal you agreed to. The key issue is whether you accept those terms by signing.

What if the dealer says it was just a system mistake?

Dealer Changed Vehicle Price on Final Purchase Contract should still be treated seriously even if the explanation is a system error. If the number is wrong, the contract should be corrected before you sign anything.

What number matters most at closing?

The vehicle selling price line matters more than the monthly payment because it affects the real cost of the transaction. Payment can be adjusted in ways that hide a higher total price.

Should I leave if they refuse to fix it?

If the dealer refuses to produce a contract that matches the agreed deal, leaving may be the safest option. Signing inaccurate paperwork usually creates bigger problems later.

Recommended Reading

If this situation sounds familiar, these related guides can help you compare nearby dealership contract problems and understand what may happen next:

Read this next if the price problem may actually involve financing terms shifting after the paperwork stage:

Read this next if the issue moved beyond the final contract stage and the vehicle price changed after signing:

Dealer Changed Vehicle Price on Final Purchase Contract is the kind of moment that tests whether you are still reviewing the deal or simply being pushed through it. The room may feel routine. The finance manager may keep talking like nothing important has changed. But once that higher number appears in the contract, the entire transaction has to stop until it is explained and corrected.

Do not sign around the problem. Do not assume the paperwork will be fixed later. Put the contract down, compare the numbers, and require a corrected version before the deal moves one inch further. If the vehicle price in the final purchase contract is wrong, the only safe move is to stop the process immediately and force the paperwork back to the real agreement.